Vertical Fintech: Rebuilding Industry-Specific Financial Infrastructure for the Digital Age

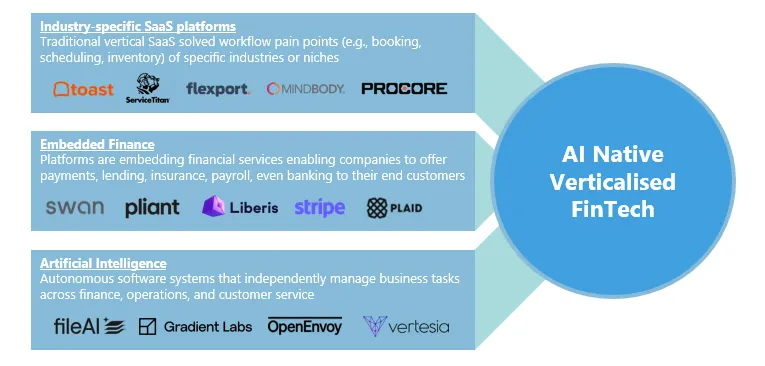

A Perfect Storm: Vertical SaaS, Embedded Finance, and AI

Every plumber, retailer, and clinic is quietly becoming a fintech company and they don’t even know it yet. That’s the power of vertical fintech where SaaS, finance, and AI converge.

- Industry-Specific SaaS Platforms: Companies like Toast (restaurants), ServiceTitan (field services), and Shopify (e-commerce) started as operational tools but quickly layered financial services such as payments, lending, and insurance, turning into critical economic arteries within their verticals.

- Embedded Finance Infrastructure: The maturation of APIs, BaaS platforms, and open banking has dramatically lowered barriers to embed financial services directly into vertical workflows. Firms like Stripe, Adyen, and Marqeta have built the rails that power this embedded ecosystem.

- AI Breakthroughs: AI-driven automation, predictive analytics, and autonomous agents now perform complex, context-sensitive tasks — reconciliation, risk underwriting, cash flow prediction — at scale, fundamentally augmenting the operating leverage of vertical fintechs.

The result is a new kind of business: vertical fintech — financially intelligent software platforms that sit at the heart of industry operations and financial flows.

Why Horizontal Solutions Left Some Industries Behind

While horizontal fintech and SaaS platforms have powered broad innovation in areas like payments, accounting, and payroll, they were never designed to serve the nuanced, fragmented, and compliance-heavy workflows of most industries.

Industries like construction, logistics, healthcare, and field services operate with:

- Highly specific workflows (e.g. permitting, claims, inspections, certifications),

- Offline or hybrid operational models, where tools must bridge physical and digital, and

- Unique financial behaviors, such as milestone-based payments, tip credits, or shared revenue splits.

In contrast, vertical fintech platforms embed within the operating rhythm of the business. They’re designed with local context, regulatory nuance, and frontline UX in mind, which is why they win both usage and economics.

This is why many large horizontal players now partner with or acquire vertical specialists: because depth is the new moat.

The Infrastructure Layer Is Built: Vertical Platforms Are Building on Top

Over the past decade, fintech infrastructure has matured from “developer-first APIs” to full-stack, white-labeled solutions. Platforms like Stripe, Adyen, Marqeta, Lithic, Unit, and Parafin have built the rails for:

- Payments processing

- Card issuance

- Lending and credit underwriting

- Banking-as-a-Service

- Embedded insurance

What once required licenses, compliance teams, and capital now requires… an integration.

This has unlocked a flood of innovation. Vertical SaaS companies — from restaurant POS systems (Toast) to e-commerce builders (Shopify) to field service apps (ServiceTitan) — have layered fintech into their workflows and, in many cases, turned financial services into their primary business model.

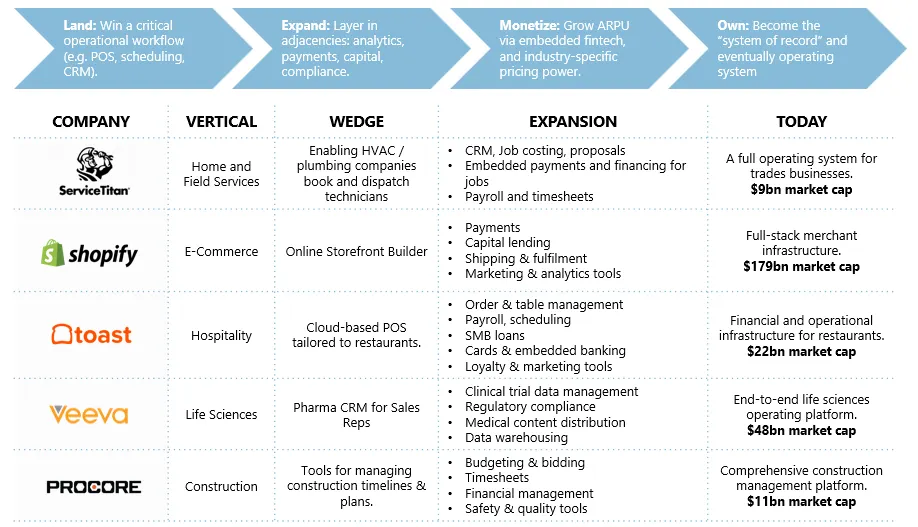

From Workflow Tools to Financial Operating Systems

The success of vertical fintech isn’t just about monetization. It’s about re-architecture.

A traditional vertical SaaS might have been a workflow tool — used daily but limited in value extraction. A vertical fintech platform is:

- More deeply embedded in daily operations (e.g. payments, payroll, capital),

- Built on proprietary, real-time financial data, and

- Able to upsell mission-critical products that increase ARPU and retention.

Winning platforms follow a common playbook:

This progression results in lower CAC, higher NRR, and deeper moats.

AI Is the Third Layer: The Rise of Vertical Agents

If embedded finance was the second wave in vertical SaaS, AI is the third.

Industry-specific platforms now sit on proprietary operational + financial data, making them uniquely well-positioned to deploy AI agents that can:

- Reconcile accounts,

- Predict cash flow,

- Automate compliance,

- Underwrite risk, and

- Optimize inventory or workforce planning.

These platforms are evolving into autonomous operators, not just tools, but partners in decision-making.

Early data is compelling: vertical platforms adopting AI report 70%+ time savings in feature development and 2–10x improvements in revenue per customer.

What We Look for at Illuminate

At Illuminate, we’ve long been interested in category-defining platforms at the intersection of financial infrastructure and vertical intelligence.

When we evaluate vertical fintech opportunities, we ask:

- Does this platform own a mission-critical workflow in a fragmented but valuable industry?

- Can it layer in embedded financial services with clear monetization pathways?

- Is the data loop strong enough to support automation, underwriting, and AI agents?

- Are there tailwinds from regulation, complexity, or distribution that create defensibility?

In this emerging stack, vertical platforms are no longer just SaaS tools. They are data-rich, financially embedded, AI-native industry networks — and they’re just getting started.

The next decade of fintech won’t be about banks or apps, it’ll be about industries quietly turning into financial ecosystems. That’s where long-term winners emerge. If you’re building in that direction, we’d love to connect.

.png)